New Delhi: As Prime Minister Narendra Modi prepares to surpass Jawaharlal Nehru as India’s longest-serving continuously elected prime minister, the milestone has sparked renewed attention on the country’s economic transformation over the past 12 years.

Since taking office in 2014, Modi has overseen a period marked by rapid infrastructure development, digital innovation, expanded welfare coverage, and significant economic growth. However, challenges related to manufacturing and employment continue to remain key policy priorities.

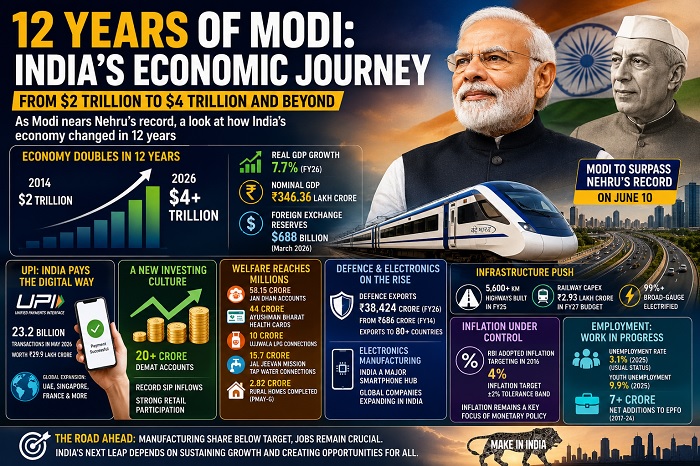

Economy Doubles in Size

India’s economy has grown from approximately $2 trillion in 2014 to more than $4 trillion in 2026, making it one of the fastest-growing major economies in the world.

According to official estimates, real GDP growth reached 7.7 percent in FY26, while nominal GDP rose to ₹346.36 lakh crore. Foreign exchange reserves also climbed to nearly $688 billion, reflecting the country’s stronger macroeconomic position.

Infrastructure Push Drives Growth

Infrastructure development has emerged as a cornerstone of the government’s economic strategy.

Thousands of kilometres of highways have been constructed over the past decade, while Indian Railways has received record capital investments. Broad-gauge railway electrification has crossed 99 percent, and 164 Vande Bharat trains are currently operational across the country.

The government has consistently increased public capital expenditure, focusing on roads, railways, ports, airports, and logistics networks to boost long-term economic capacity.

UPI Revolutionizes Digital Payments

One of the most visible transformations has been the rise of the Unified Payments Interface (UPI).

According to the National Payments Corporation of India (NPCI), UPI processed a record 23.2 billion transactions worth ₹29.9 lakh crore in May 2026. The platform has become an integral part of daily commerce and expanded internationally to countries including the UAE, Singapore, and France.

Rise of Retail Investors

India has also witnessed a dramatic increase in retail participation in financial markets.

Demat accounts have crossed 20 crore, while monthly SIP investments in mutual funds continue to hit record levels. Domestic investors now play a much larger role in supporting stock markets and reducing dependence on foreign capital flows.

Welfare Programs Reach Millions

Financial inclusion and social welfare have expanded significantly under various government initiatives.

Jan Dhan accounts have crossed 58 crore, while health coverage under Ayushman Bharat has reached approximately 44 crore beneficiaries. Schemes such as Ujjwala, Jal Jeevan Mission, and PMAY-Gramin have extended benefits to millions of households across the country.

Manufacturing and Defence Exports Gain Ground

India has made notable progress in electronics production and defence exports.

Defence exports have increased from ₹686 crore in FY14 to a record ₹38,424 crore in FY26. The country now exports defence products to more than 80 nations.

Electronics manufacturing has also expanded, with India emerging as a major smartphone production hub as global companies increase investments in domestic supply chains.

Employment and Manufacturing Remain Focus Areas

Despite the progress, manufacturing continues to account for a smaller share of GDP than the government’s long-term target.

The Make in India initiative initially aimed to raise manufacturing’s contribution to 25 percent of GDP, but current estimates place it below that level. Employment generation also remains closely monitored as India’s workforce continues to grow.

The Bigger Picture

Twelve years after Modi first assumed office, India is larger economically, more digitally connected, financially integrated, and infrastructure-focused than it was in 2014.

While achievements such as GDP growth, UPI adoption, welfare expansion, and infrastructure development stand out, manufacturing growth and job creation remain critical areas that will shape India’s next phase of economic development.